That majority-control requirement is the key. A regular spinoff separates a business and leaves it independent. A Reverse Morris Trust is used when the parent wants something closer to sale economics — moving the business to a buyer — without creating the same corporate tax bill as a straightforward asset sale.

The structure is powerful, but it is not simple. It usually requires a tax-free spinoff, a pre-arranged merger, careful ownership math, and a buyer that is the right size. If the parent company’s shareholders do not end up with more than 50% of the combined company, the tax treatment can change.

This guide explains how Reverse Morris Trust transactions work, why companies use them, where they can go wrong, and how they differ from ordinary spinoffs.

In plain English: A Reverse Morris Trust is a way for a company to get rid of a division by combining it with another company, while structuring the deal so the parent’s shareholders still control the merged business.

What Is A Reverse Morris Trust?

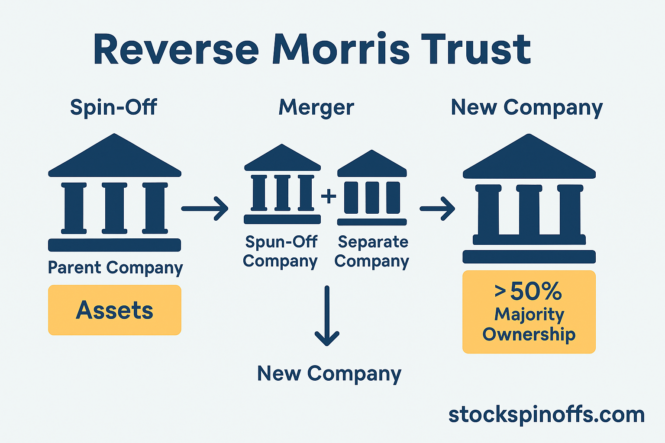

A Reverse Morris Trust, often shortened to RMT, is a two-step corporate transaction.

- The parent company spins off a subsidiary to its own shareholders, usually in a transaction intended to qualify as tax-free under Section 355 of the Internal Revenue Code.

- The spun-off company then merges with a third-party buyer. To preserve the intended tax treatment, the former parent company’s shareholders generally must own more than 50% of the combined company after the merger.

That is why an RMT can look like a sale but behave differently for tax purposes. The parent is effectively divesting a business, but the parent’s shareholders remain the majority owners of the combined company.

For background on the older structure and history, see our prior primer: Reverse Morris Trust – What Is It And What Is It Used For?

Key concept:

- Regular spin-off: Parent distributes shares to shareholders tax-free, but the business remains independent.

- RMT: Enables a sale to another company without taxes by ensuring the parent’s shareholders retain control post-merger.

For background, see our prior primer: Reverse Morris Trust – What Is It And What Is It Used For? (2017).

How A Reverse Morris Trust Works

The mechanics are easiest to understand as a sequence.

- Parent identifies a business to separate. The parent company decides that a division or subsidiary no longer fits its strategy.

- Parent creates SpinCo. The business is placed into a new company.

- Parent distributes SpinCo to shareholders. Parent shareholders receive shares of SpinCo, typically in a tax-free spinoff.

- SpinCo merges with a buyer. The spun-off company combines with a third-party company.

- Parent shareholders keep control. The former parent company’s shareholders must generally own more than 50% of the combined company.

Example: Company A wants to separate Division X. It spins Division X into SpinCo and distributes SpinCo shares to Company A shareholders. SpinCo then merges with Company B. If Company A shareholders own about 51% of the combined SpinCo/Company B business, the transaction may qualify as a Reverse Morris Trust.

The practical result is that Company A has separated Division X and combined it with a buyer, while avoiding the tax treatment that might apply to a direct sale.

Why Companies Use Reverse Morris Trusts

Companies use Reverse Morris Trusts because they can solve a problem that ordinary spinoffs and asset sales do not.

- A direct sale can create tax leakage. Selling a division for cash may trigger corporate tax.

- A regular spinoff may not create the right owner. The business may be better combined with an industry buyer than left as a standalone public company.

- The parent can sometimes receive cash. SpinCo may borrow money and pay a dividend to the parent before the merger.

- Shareholders keep upside. Parent shareholders usually receive ownership in the combined business rather than being cashed out entirely.

- The buyer can gain scale. The buyer gets a business it wants, often without paying all cash.

The attraction is obvious. The parent can divest a business, shareholders can retain exposure, and the transaction may avoid the tax cost of a simpler sale.

The catch is that the structure has to be done correctly.

Where Reverse Morris Trusts Can Go Wrong

RMTs are not magic. They are complicated transactions with several constraints.

- The ownership math matters. Former parent company shareholders generally need to own more than 50% of the combined company.

- The buyer cannot be too large. If the buyer is too big, it may be hard for the parent company’s shareholders to retain majority ownership after the merger.

- The tax rules are technical. The transaction must be structured carefully to avoid losing the intended tax treatment.

- The deal can be expensive and slow. RMTs require legal, tax, accounting, and regulatory work.

- The combined company still has to make business sense. A tax-efficient deal can still be a bad strategic merger.

That last point is easy to overlook. The tax savings may get the deal announced. The business fit determines whether shareholders should be happy about it later.

Notable Examples

- Lockheed Martin & Leidos (2016): Lockheed spun off its IT division and merged it with Leidos. Lockheed shareholders retained 50.5%, plus $1.8B cash. (Detailed analysis: Lockheed-Martin reverse Morris Trust with Leidos, within the primer link.)

- GE & Wabtec (2019): GE’s structure was altered, making Wabtec the majority, voiding RMT status and creating a taxable event for GE and its shareholders. (See: GE restructures Wabtec deal out of RMT)

- CBS Radio & Entercom (2017): CBS Radio merged into Entercom via an RMT, with CBS shareholders owning ~72% afterward. (See: CBS Radio to merge with Entercom in RMT transaction)

- Henry Schein & Covetrus (2019): HPE spun off Covetrus and merged it via RMT with Vets First Choice, delivering $1.1B in tax-free cash to Henry Schein. (See: Henry Schein completes spinoff of Covetrus via RMT)

- AT&T & Discovery (2022): AT&T spun off WarnerMedia and merged with Discovery to form Warner Bros. Discovery, with AT&T shareholders holding ~71%—a textbook RMT.

What to notice in RMT examples: the buyer is usually not simply writing a check. The structure is designed so the parent company’s shareholders own the majority of the combined company after the spin-and-merge transaction. That ownership math is what makes the Reverse Morris Trust different from an ordinary sale.

Reverse Morris Trust vs. Regular Spinoff vs. Classic Morris Trust

| Structure | What Happens | Why Companies Use It |

|---|---|---|

| Regular spinoff | Parent distributes shares of a subsidiary to its shareholders, and the new company trades separately. | To create a standalone public company and separate businesses with different strategies or investor bases. |

| Reverse Morris Trust | Parent spins off a business, and that spun-off company merges with a third-party buyer. Parent shareholders keep majority control of the combined company. | To transfer a business to a buyer in a tax-efficient way while preserving shareholder ownership. |

| Classic Morris Trust | An older structure involving a spinoff and merger, but with the parent merging rather than the spun-off business. | Historically used for tax-efficient divestitures, but now less common after legal and tax-rule developments. |

Reverse Morris Trust FAQ

Do shareholders pay tax in a Reverse Morris Trust?

Usually not at closing if the transaction qualifies for tax-free treatment. Shareholders generally receive stock in the spun-off or combined company and may owe tax later if they sell. Individual tax treatment can vary, so shareholders should read the company’s tax disclosure and consult a tax adviser.

Why does the more-than-50% ownership test matter?

The majority-control requirement is what helps distinguish a Reverse Morris Trust from a taxable sale. If the parent company’s shareholders do not own more than 50% of the combined business, the intended tax-free treatment may be at risk.

Why not use a Reverse Morris Trust for every divestiture?

Because RMTs are complex, expensive, and only work in certain situations. The buyer has to be the right size, the business has to be suitable for a merger, and the transaction has to satisfy technical tax requirements.

Is a Reverse Morris Trust good for shareholders?

It can be, but the structure alone is not enough. Shareholders should look at the quality of the business being separated, the valuation of the merger, the debt placed on the spun-off company, and whether the combined company has a sensible strategy.

How common are Reverse Morris Trusts?

They are relatively rare. Companies usually use them only when the value of the business and potential tax savings are large enough to justify the complexity.

The Reverse Morris Trust Tradeoff

A Reverse Morris Trust can be one of the most useful tools in corporate restructuring. It lets a parent company separate a business, combine it with a buyer, and potentially avoid the tax cost of a direct sale.

But the structure is not the investment case.

For investors, the real questions are more practical: What business is being separated? What is it worth? How much debt is going with it? Who will control the combined company? And does the merger make the business better, or just tax-efficient?

That is why RMTs are worth watching closely. They can create real value, but they can also hide a lot of complexity behind the phrase “tax-free transaction.”

Related spinoff terms:

Mentions