Reverse Morris Trust: How Companies Sell Divisions Tax-Free

A Reverse Morris Trust (RMT) is a specialized, tax-efficient structure that lets a company effectively sell a business to a third party without incurring corporate tax, by pairing a tax-free spin-off with a merger in which the original parent’s shareholders end up with majority control of the combined company. Put differently: plain spin-offs are already tax-free distributions to shareholders; an RMT is used when the parent wants the sale economics (handing the business to an outside buyer) without the sale tax bill.

This guide explains what an RMT is, how it works step by step, benefits and limitations, and notable examples, plus a quick comparison with regular spin-offs and classic Morris Trusts.

What is a Reverse Morris Trust?

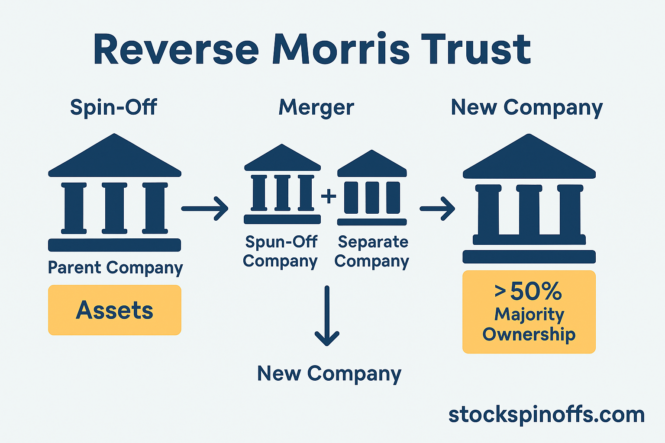

A Reverse Morris Trust is a two-step reorganization: the parent first spins off a subsidiary to its own shareholders (tax-free under IRC §355), then that newly independent SpinCo immediately merges with a third-party acquirer. If, after the merger, the former parent’s shareholders own >50% of the combined company, the transaction is treated as a tax-free reorganization rather than a taxable sale. Its naming traces back to the Mary Archer W. Morris Trust case and later legal developments.

Key concept:

- Regular spin-off: Parent distributes shares to shareholders tax-free, but the business remains independent.

- RMT: Enables a sale to another company without taxes by ensuring the parent’s shareholders retain control post-merger.

For background, see our prior primer: Reverse Morris Trust – What Is It And What Is It Used For? (2017).

How It Works

- Spin-Off (tax-free): Parent puts the business into a new entity, SpinCo, distributes its shares to shareholders.

- Pre-arranged Merger: SpinCo merges immediately with a third-party acquirer.

- Majority Test: The parent’s shareholders must own >50% of the resulting entity, preserving tax-free status.

Example: Company A spins off Division X to SpinCo, then SpinCo merges with Company B. If A’s shareholders hold ~51% of the new merged company, the structure qualifies as an RMT—avoiding taxes like a sale but functionally transferring assets.

Benefits

- Tax-free divestiture to a buyer

- Pre-merger cash to parent, often via SpinCo debt distribution

- Strategic mergers and synergies

- Shareholder value retention via deferred tax and growth upside

Requirements & Limitations

- >50% ownership required

- Spin and merger must integrate; avoid triggering §355(e) anti-abuse rules

- Structurally complex and costly

- Buyer must be modest enough in size to respect majority ownership

Notable Examples

- Lockheed Martin & Leidos (2016): Lockheed spun off its IT division and merged it with Leidos. Lockheed shareholders retained 50.5%, plus $1.8B cash. (Detailed analysis: Lockheed-Martin reverse Morris Trust with Leidos, within the primer link.)

- GE & Wabtec (2019): GE’s structure was altered, making Wabtec the majority, voiding RMT status and creating a taxable event for GE and its shareholders. (See: GE restructures Wabtec deal out of RMT)

- CBS Radio & Entercom (2017): CBS Radio merged into Entercom via an RMT, with CBS shareholders owning ~72% afterward. (See: CBS Radio to merge with Entercom in RMT transaction)

- Henry Schein & Covetrus (2019): HPE spun off Covetrus and merged it via RMT with Vets First Choice, delivering $1.1B in tax-free cash to Henry Schein. (See: Henry Schein completes spinoff of Covetrus via RMT)

- AT&T & Discovery (2022): AT&T spun off WarnerMedia and merged with Discovery to form Warner Bros. Discovery, with AT&T shareholders holding ~71%—a textbook RMT.

RMT vs. Spin-Off vs. Classic Morris Trust

| Structure | Description |

|---|---|

| Standard Spin-Off | Tax-free distribution; business remains standalone |

| Reverse Morris Trust | Tax-free sale to a buyer via spin + merger, with shareholder control maintained |

| Classic Morris Trust | Older structure where parent merges post-spin; less common now |

Frequently Asked Questions

Do shareholders pay tax?

Not at closing—tax is typically deferred unless they later sell inherited shares.

Why >50% is important?

It’s the IRS’s test for a reorganization, not a taxable sale.

Why not always use RMTs?

Complex, expensive, buyer must be appropriately sized and willing.

How common are RMTs?

Rare; usually deployed when value and tax savings are substantial.

The Reverse Morris Trust Advantage—and Its Risks

A Reverse Morris Trust enables a company to sell a division tax-free, while keeping shareholder control through majority ownership.

But proceed with caution: the structure, timing, and deal terms must be precise—lapse on the ownership threshold and you trigger taxation. RMTs offer powerful tax outcomes—but only if executed flawlessly.

Mentions